Never Reason from a Velocity Change

Never Reason from a Velocity Change

or "how I learned to stop worrying and wait for deflation"

As some of you may know, my glasses literally say MV = PY on the side. I feel like that’s pretty strong evidence to show that I’m sympathetic toward the Equation of Exchange and its uses.

This is why I’m always pissed off when I hear someone say that “inflation is high because velocity is increasing” or that “raising the money supply was necessary because velocity fell.”

OK, fine. Let me start over. Remember that MV = PY is a tautology since V is defined as PY/M. Now let’s think about a central bank which is trying to stabilize NGDP or the price level. We would expect it to “cancel out” changes in velocity by changing the money supply. That way, it can keep PY constant.

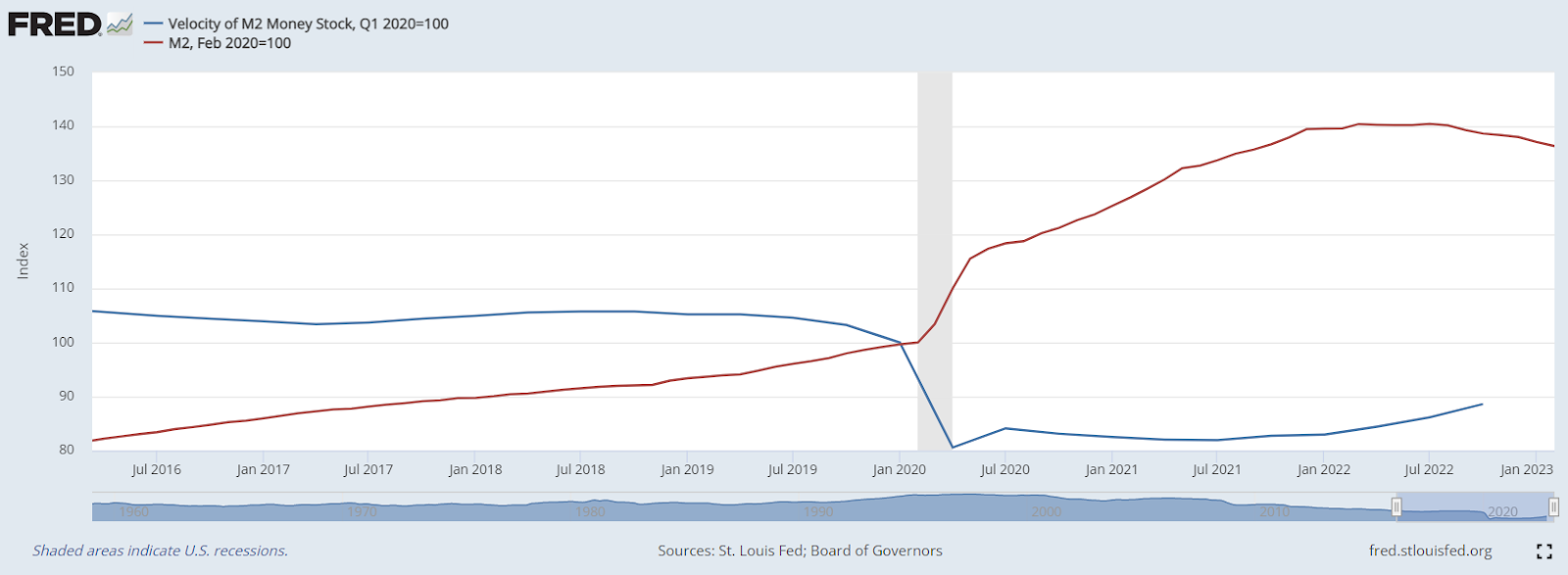

So, if we put velocity and the money supply on the same graph, we should see that they have an inverse relationship.

And they do! In 2020, velocity fell, and the money supply rose. The opposite has been happening recently, i.e. velocity has been rising but the money supply has been falling. Damn, seems like the Fed is doing its job correctly!

But...let me present to you a somewhat different thesis. (1) Velocity is roughly constant over time or at least has a long-run trend, and (2) increases in the money supply require time to affect the price level or NGDP. In other words, there are long and variable lags in monetary policy. These two theses are commonly known as, you know, monetarism. The school of thought which actually cares about velocity, because it believes that velocity has structural determinants in the long-run. Other schools of thought tend to view velocity as an useless measure, as it’s literally a residual. Meaning that velocity just captures whatever changes in PY aren’t captured by changes in M. For those critical of monetarism, velocity here is just a tautological way of validating the theory.

So I’m guessing that if you’ve ever said something to the effect of “Fed had to raise M in 2020 because velocity fell” or “it’s fine that the money supply is falling now because velocity is rising,” then you’re somewhat sympathetic to monetarism and the two assumptions underlying it that I’ve mentioned above.

So let’s think about 2020 and 2023 in terms of those assumptions. If “printing money” takes time to affect nominal GDP, then an immediate and large increase in M (like we saw in 2020) will not increase PY. But remember that MV = PY is an equation. It must hold. So if you have a large increase in M, which leaves PY unchanged (at least in the short run), then V will fall. So another way to think about it is that the Fed did not raise M in response to a fall in V but *caused V to fall*.

This point, by the way, is even more likely if you believe the Krugman take on the liquidity trap. Under this argument, if you’re at the zero lower bound, then increasing M will not affect P or Y. And since we were at the zero lower bound in 2020, this model would predict that increasing M…causes V to fall.

Likewise, imagine a scenario where you *decrease* the money supply, as has happened over the last few months (dear reader, I recognize that money is “endogenous” and that the Fed sets rates, but you know what I mean here), then if we buy into the “long and variable lags” idea, velocity would rise (because, again, PY doesn’t react fast enough, so V must). So, one could argue that the recent rise in velocity is *caused by the decrease in M*.

And if this is true, then the fall in M will *eventually* lead to a decrease in PY and cause a massive recession. And this will only come after the 2020 rise in M is fully absorbed into the price level. In other words, we could be in for a fun two years when inflation suddenly goes from 4% to -2%. Don’t take it from me; look at Lars Christensen’s simulation (who, by the way, saw our recent inflation coming back in April 2021).

But anyway, this could all be false. Monetarism is a weird theory exactly because we haven’t figured out how V works. But please heed my words; if you think V is important, then never reason from a velocity change. They will more often than not be caused by changes in the money supply needing time to show up in NGDP.

Sandro, I feel as I was the "target" of your critique. Anyway, Friedman´s "Thermostat Analogy" "looks" at the equation of exchange and sees the Fed´s job as controlling the thermostat (Money supply growth) so as to compensate changes in the "outside temperature" (Velocity) in order to maintain the "Inside temperature" (NGDP growth) stable. Since the mid 1980s, and for long streches of time that´s exactly what happened (Great Moderation was the result). It failed miserably in 2008/09 (Great Recession) and for the next decade managed to keep the "inside temperature" stable at a lower (but stable) temperature! The Fed reacted appropriately to the C-19 shock, leading to the shortest recession on record (2 mos) and also the fastest recovery. The it failed to adjust the thermostat so the economy (NGDP) heated up!

Some illustrations here: https://marcusnunes.substack.com/p/when-monetary-policy-tightening-is

And this is a nice exposition by Nick Rowe: https://worthwhile.typepad.com/worthwhile_canadian_initi/2010/12/milton-friedmans-thermostat.html