A Monetarist Retrospective on Inflation

A Monetarist Retrospective on Inflation

Is it supply, demand or a secret third?

The last two years have created a three-question litmus test for any macroeconomic theory or model. They are as follows:

Why was the recovery from 2008 so slow, but the recovery from the pandemic so rapid, especially since the Fed conducted QE in both cases?

Why did inflation explode after Covid, is this a supply-side or demand-side phenomenon? To what degree is it one or the other?

How will inflation end?

Those of us who believe in something akin to market monetarism have fairly exact answers to all three of these questions.

Question 1: The Recovery

The post-pandemic recovery was, indeed, incredible. In April 2020 unemployment peaked at 14.7%. In a year it had come down to 6%, and in two years unemployment was just 3.6%.

Compare this to the period following the Great Financial Crisis, when unemployment reached a peak of 10% in October 2009 and took almost 9 years to drop below 4% in May 2018. The question of why standard macroeconomics failed so badly in the post-GFC period plagued economists, especially since the Fed was chaired by Ben Bernanke, who had written about an eerily similar problem in Japan. In fact, it seemed like monetarism was the macroeconomic approach that took the biggest hit. Despite several rounds of quantitative easing and a quadrupling of the monetary base, inflation continued to stay below target.

But for a few true believers, everything seemed to make sense. Quantitative easing could be good, but it had to have a goal. The Federal Reserve needed to commit to a certain policy objective and say that it would do “whatever it takes” to achieve that. Furthermore, inflation targeting wasn’t enough. Even if the Fed conducted inflationary policy, if the public really believed in the 2% target, they would expect the Fed to later tighten policy in response to high inflation. To truly succeed, a central bank has to commit to be irresponsible.

And that’s what happened in 2020. The Federal Reserve introduced a system of “flexible average inflation targeting”. Because inflation had been below target for so long, the Fed would now allow it to go above target for a certain period of time, to achieve the policy goal of averaging 2% over the long-run. A rapid recovery ensued.

And then came above “above target” inflation.

Question 2: Inflation

This is a weird one. Particularly because monetarists have a few different ways of saying “I told you so!”. The first, most obvious, but somewhat incorrect assertion would be to say that inflation is primarily linked to broad money and not the monetary base. The post-GFC Fed failed in significantly affecting broad monetary aggregates such as M2, while the Powell Fed managed to raise M2 by 40% over two years. So, from a naïve monetarist standpoint, it would have been insane to not expect huge inflation.

But that’s still an imperfect explanation as it doesn’t say why broad money didn’t expand after the GFC. It’s also lackluster as the post-Covid inflation is much lower than would be predicted by a 40% expansion of M2.

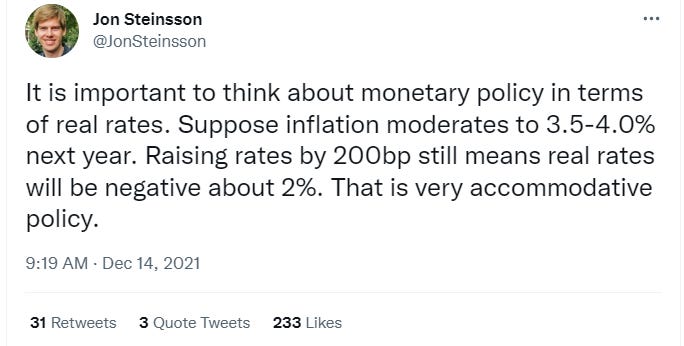

The more “market monetarist” explanation would start with a Jon Steinsson Tweet from a year ago.

In essence, monetary policy was loose in late 2021. It was extremely loose. Despite inflation expectations being above target, the Federal Funds Rate was at 0% and QE was still ongoing. This made zero sense. Nevertheless, others persisted in claiming that inflation was just from a supply shock. Covid had disrupted supply chains, China was still in lockdown, and this was all before the eruption of the single biggest conflict since World War 2.

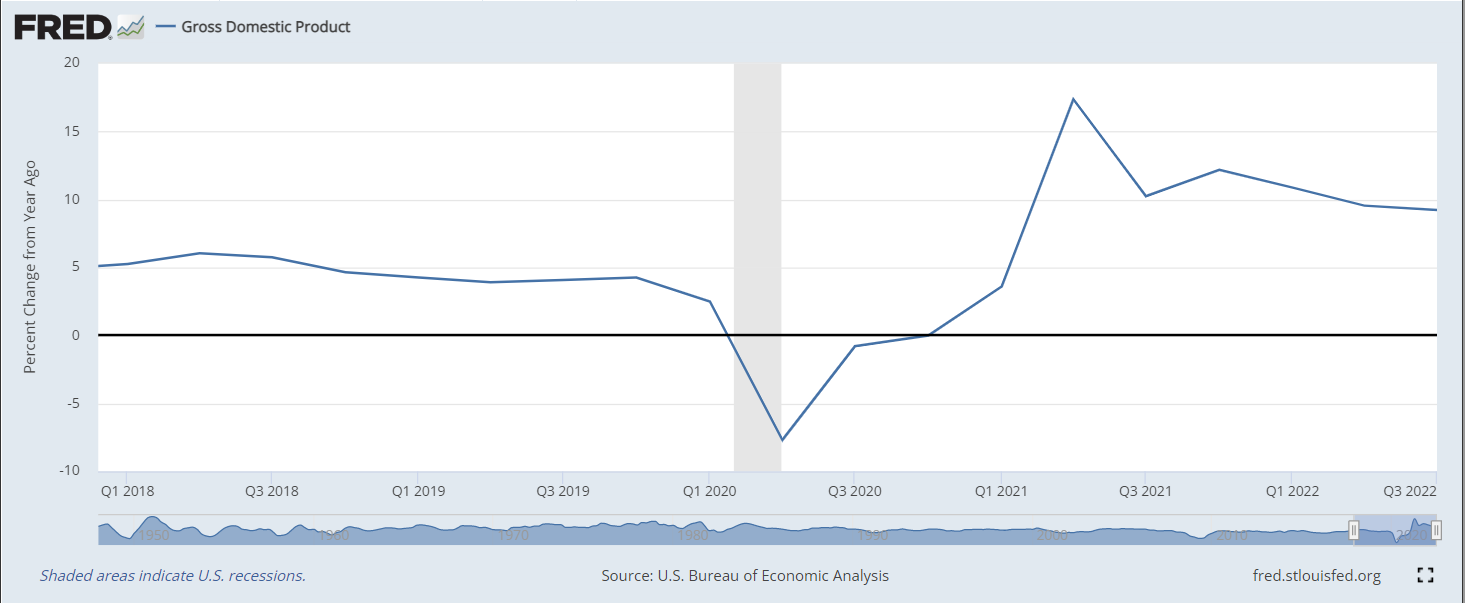

Nevertheless, if one followed standard market monetarist thinking, things did not add up. By any reasonable estimate, NGDP was back on its normal growth trend midway through 2021, but it kept rising at double-digit rates in the following quarters. It is indeed possible for a supply shock to raise NGDP if it raises prices more than it lowers real GDP, but it is not possible for a pure supply shock to give you double-digit NGDP growth when your “usual” growth rate is just 4%.

Oh and the Fed knew. Federal Reserve forecasts showed nominal GDP going above trend as early as quarter 3 of 2021. So fairly basic market monetarist principles explained inflation as primarily demand-driven and prescribed the policy of higher interest rates.

Question 3: The Landing

The biggest worry that people have now is the fight against inflation. Will a recession, a rise in unemployment, and a period of suffering be necessary? The monetarist take here is “probably not, and if so, it won’t be that bad”.

This, naturally, invites the question of “but what about the Volcker shock? It was a huge recession!”. This observation is indeed correct, but misses the primary mechanism by which higher rates raise unemployment.

Imagine you are a firm expecting 10% inflation. You promise your workers a 10% raise. Suddenly, the Fed starts tightening policy, inflation only comes out at 2%. Your revenue rises only by 2%, so you can’t afford to give your workers a 10% raise. You fire them, causing unemployment.

But what if you only expected 2% inflation to begin with? Then the Fed’s goal would not be too far off from what you based your expectations on. Unemployment need not rise as much. Inflation can go down without a severe recession.

This is where we are now. The 5-year TIPS spread (my preferred metric of inflation expectations) is at around 2.3%. This tells me that inflation can go down without a severe recession. Perhaps we’ll experience a rise in unemployment, but I would not expect it to rise higher than 5%. And though a 1.5pp rise would definitely be a significant issue, it is not comparable to the double-digit unemployment of the Volcker years. This is the last “out of sample” prediction that market monetarism is making for the post-Covid period.